Peter Lynch — The Magician Who Made Mutual Fund Math Look Easy

Trends shift, but one principle stays constant: simplicity. The brands that win are the ones that make things clear, timeless, and easy to connect with.

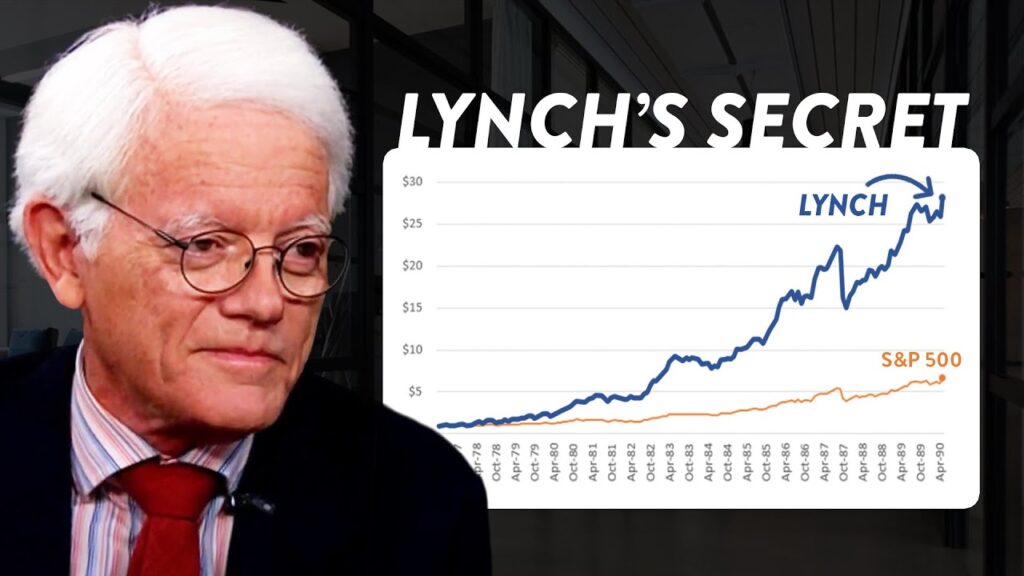

Picture this: you take over a tiny fund in 1977, pour common-sense observation into every buy decision, and by 1990 you’ve transformed it into one of the world’s most watched funds — producing an average annual return of about 29.2% and growing assets from roughly $18 million to ~$14 billion. That’s the Peter Lynch story: disciplined, plainspoken, and bracingly practical.

The core mindset

Lynch’s method is equal parts curiosity and classification. Read his playbook in One Up On Wall Street and Beating the Street: invest in what you understand, then do the homework. He popularized ideas that anyone — not just PhD quants — can use: spot everyday trends, understand a company’s economics, and buy when the price is attractive.

Signature tactics (short and punchy)

“Invest in what you know.” If you notice a product or service gaining traction in real life — at work, at the mall, online — that’s a lead, not a rumor.

Categorize every stock. Lynch split equities into types (fast growers, stalwarts, cyclicals, asset plays, turnarounds, slow growers). That category decides how you value and hold it.

Tenbagger hunting. He chased “tenbaggers” — stocks that deliver 10× gains — knowing a few big winners can propel a portfolio over years (typical holding horizon: 3–10 years for big payoffs).

Do the math, simply. He liked plain metrics: earnings growth, PEG ratio (price/earnings to growth), and free cash flow. If the story doesn’t add up in numbers, don’t buy.

Scuttlebutt research. Talk to customers, suppliers, store managers — grassroots intel often beats headline analysis.

Cut losers fast, let winners run. He sold quickly when fundamentals failed, but he didn’t panic-sell winners.

Why it worked (and when it fails)

Lynch’s edge was putting retail-level observation into institutional-sized bets while remaining numerate and humble. He ran the Fidelity Magellan Fund with a mix of concentration and diversification — holding many good ideas but willing to overweight his best convictions. The approach flounders when one confuses fad-spotting with durable revenue growth, or when emotion crowds out math.

Intellectual roots

Lynch sits in a lineage that includes value thinkers like Benjamin Graham, but he made value practical and modern: growth that’s understandable and priced sensibly.